Chapter 3 Linear Regression

What is linear regression?

- “a very simple approach for supervised learning”

- “a useful tool for predicting a quantitative response”

- widely used statistical learning method

- a special case of more generalized learning methods

- Useful for answering many different types of questions

Advantages

- Simplicity

- Conceptual: based on averages (or “expectations” in econometrics)

- Procedural: there are closed form solutions for estimating parameters

- Interpretable

- There are meaningful visualizations and interpretations of model results

- It is possible to address many types of questions, and apply statistical tests to judge results including:

- Is there a relationship between predictors and response variables?

- How strong is the relationship?

- Which predictors are related to the response?

- How accurate are the estimated model parameters?

- How accurate are the predictions generated by the model?

- Is the model a good fit?

- Are there interactions among the predictors?

3.1 Simple linear regression

Simple linear regression predicts a quantitative response \(y\) on the basis of a single predictor, \(x\), assuming that there is a linear relationship between \(y\) and \(x\) in the form:

\[ \begin{array}{rcl} y &=& \beta_0 + \beta_{1}x + \epsilon \\ &\textrm{or}& \\ y &\approx& \beta_0 + \beta_{1}x \end{array} \]

Read as: “regressing \(y\) on \(x\)”, “regressing \(y\) onto \(x\)”, or “\(y\) is approximately modeled as a linear function of \(x\)”

This equation describes the population regression line: the best linear approximation of the true relationship between \(y\) and \(x\). The model parameters (or coefficients), \(\beta_0\) and \(\beta_1\), are unknown constants and the error term, \(\epsilon\), is not measurable in practice.

- \(y\): the observed true value of \(y\)

- \(\beta_0\): the intercept, or the expected value of \(y\), when \(x\) is 0

- \(\beta_1\): the slope, or the expected change in \(y\) per unit change in \(x\), or \(\frac{\Delta y}{\Delta x}\)

- \(\epsilon\): irreducible error, or variation in \(y\) that can not be accounted for by the model

3.1.1 Estimating Coefficients

In practice \(\beta_0\) and \(\beta_1\) are unknown constants that must be estimated based on available data using some procedure.

- Each \((x_i, y_i)\) pair represents an example observation drawn from the population of possibilities for the joint distribution of \(X\) and \(Y\).

- Based on many (\(n\)) examples, develop estimates for \(\hat{\beta}_0\) and \(\hat{\beta}_1\).

- Then compute \(\hat{y}_i\), which is the value for \(y_i\) predicted by the model based on \(x_i\) (where \(i \in \{1 \ldots n\}\)).

\[ \hat{y}_i \approx \hat{\beta}_0 + \hat{\beta}_1 x_i \]

The prediction is an approximation is unlikely to be exactly equal to the actual value. The difference is called the residual. For a particular example observation, \(i\), the residual is computed as:

\[ e_i = y_i - \hat{y}_i \]

Better estimates of the parameters \(\beta_0\) and \(\beta_1\) will yield better predictions for \(y\) and, therefore, smaller residuals. The residual sum pf squares (RSS) is a measure of the overall magnitude of the prediction error for a particular set of coefficients and training data. The lower the RSS, the better the estimates should be (assuming the model is correctly specified, etc.).

\[ \begin{array}{rcl} RSS &=& \sum_{i}^{n} e_{i}^{2} \\ &=& \sum_{i}^{n} (y_i -\hat{y}_i)^2 \\ &=& \sum_{i}^{n} (y_i - \hat{\beta}_0 + \hat{\beta}_1 x_i)^2 \end{array} \]

Minimizing the RSS is accomplished by choosing appropriate values for \(\hat{\beta}_0\) and \(\hat{\beta}_1\), which are estimates for the true (but unknown) population parameters, \(\beta_0\) and \(\beta_1\). This method is referred to as the least squares approach in the text.

3.1.2 Simulated Data Example

- model: \(y = \beta_0 + \beta_1 x + \epsilon\)

- parameters: \(\beta_0\) = 2 and \(\beta_1\) = 3.

Simulate drawing a sample from the population by generating data

# Number of observations

n <- 100

# random variable x

x <- runif(n)

# True slope and intercept of line

beta <- c(2, 3)

# irreducible error

epsilon <- rnorm(n)

# True value of y

y <- beta[1] + beta[2] * x + epsilonFirst few rows of the simulated data sample

| y | x | epsilon |

|---|---|---|

| 4.299174 | 0.8543299 | -0.2638157 |

| 1.188886 | 0.1168752 | -1.1617401 |

| 5.271001 | 0.6867674 | 1.2106981 |

| 3.357570 | 0.0163384 | 1.3085549 |

| 2.984540 | 0.3480136 | -0.0595011 |

| 4.802275 | 0.6009924 | 0.9992976 |

Minimize RSS to compute least squares estimates for \(\hat{\beta_0}\) and \(\hat{\beta_1}\)

# residual sum of squares formula

rss <- function(...) {

beta <- c(...)

sum((y - (beta[1] + beta[2] * x))^2)

}Try guessing the parameters that will minimize RSS for the sample

tibble(beta_0 = c(0, 1, 2, 1.8), beta_1 = c(1, 2, 3, 3.3)) %>%

group_by(beta_0, beta_1) %>%

mutate(RSS = rss(beta_0, beta_1)) %>%

ungroup() %>%

kable()| beta_0 | beta_1 | RSS |

|---|---|---|

| 0.0 | 1.0 | 1094.7367 |

| 1.0 | 2.0 | 363.2831 |

| 2.0 | 3.0 | 102.3890 |

| 1.8 | 3.3 | 101.1695 |

Surprisingly (perhaps) using \(\hat{\beta_0}\) = 2 and \(\hat{\beta_1}\) = 3 does not yield the lowest RSS for the sample data even though these are the exact parameters \(\beta_0\) and \(\beta_1\) used to generate the sample observations. This is because irreducible error component is not observed and our sample size is limited.

Instead of guessing we can use R to automatically choose beta to minimize RSS. The optim() can do this.

## [1] 1.778687 3.5452843.1.3 Closed-form solution

Applying some algebra and calculus to the RSS formula yields the following exact solutions for estimating \(\hat{\beta_0}\) and \(\hat{\beta_1}\) that will minimize RSS

\[ \begin{array}{rcl} \hat{\beta_1} & = & \frac{\sum_{i=1}^{n} (x_i - \bar{x})(y_i - \bar(y)) }{ \sum_{i=1}^{n} (x_i - \bar{x})^2 } \\ \hat{\beta_0} & = & \bar{y} - \hat{\beta_1}\bar{x} \\ \end{array} \]

## [1] 3.544119## [1] 1.779281Estimated model using least squares method:

\(\hat{y}\) = 1.78 + 3.54 \(x\)

We can also use the lm() function to estimate the parameters

##

## Call:

## lm(formula = y ~ x)

##

## Coefficients:

## (Intercept) x

## 1.779 3.5443.2 Assessing Accuracy of Coefficients

The goal is to estimate pthe arameters of the actual population regression function based on a sample

Since we have estimated our parameters based on a sample, there is likely to be some error.

simulate_data <- function(beta = c(0, 0), n = 100, sd = 1) {

# column dimension

m <- length(beta)

# Population parameters

beta <- matrix(beta, nrow = 1, dimnames = list(NULL, paste0("beta_", seq_along(beta)-1)))

# Sample Data

X <- matrix(

data = c(rep(1, n), # Assign a constant term for x_0

rnorm((m-1) * n, sd = sd)), # random normals for remaining x

ncol = m, nrow = n,

byrow = FALSE,

dimnames = list(NULL, paste0("x_", seq_along(beta)-1))

)

# Irreducible error

e <- matrix(rnorm(n, sd = sd), ncol = 1, dimnames = list(NULL, "e"))

# Compute y

y <- X %*% t(beta) + e

colnames(y) <- "y"

# Return a data frame, drop the constant

data.frame(cbind(y, X, e))[, -2]

}

#test <- simulate_data(beta = c(2, 3), n = 1000)

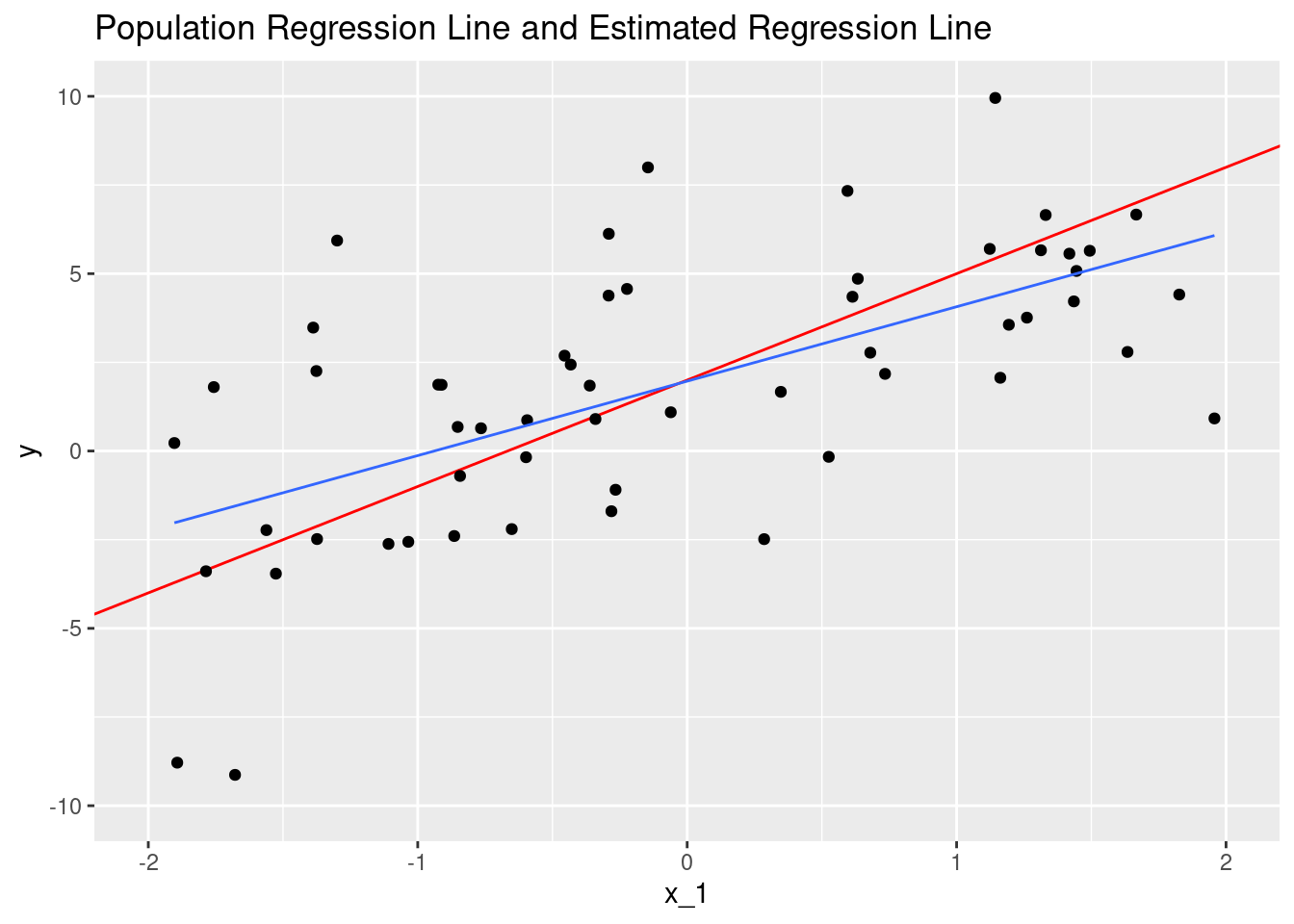

#testHere is a plot of linear function with the parameters we estimated, compared with the population regression function.

# Replicate Figure 3.3

# Generate 1 sample and plot

simulate_data(beta = c(2, 3), n = 100, sd = 3) %>%

ggplot(mapping = aes(x = x_1, y = y)) +

geom_abline(slope = 3, intercept = 2, color = "red") +

geom_point() +

geom_smooth(method = "lm", se = FALSE, size = 0.5) +

scale_x_continuous(limits = c(-2, 2)) +

scale_y_continuous(limits = c(-10, 10)) +

labs(title = "Population Regression Line and Estimated Regression Line")## `geom_smooth()` using formula 'y ~ x'## Warning: Removed 44 rows containing non-finite values (stat_smooth).## Warning: Removed 44 rows containing missing values (geom_point).

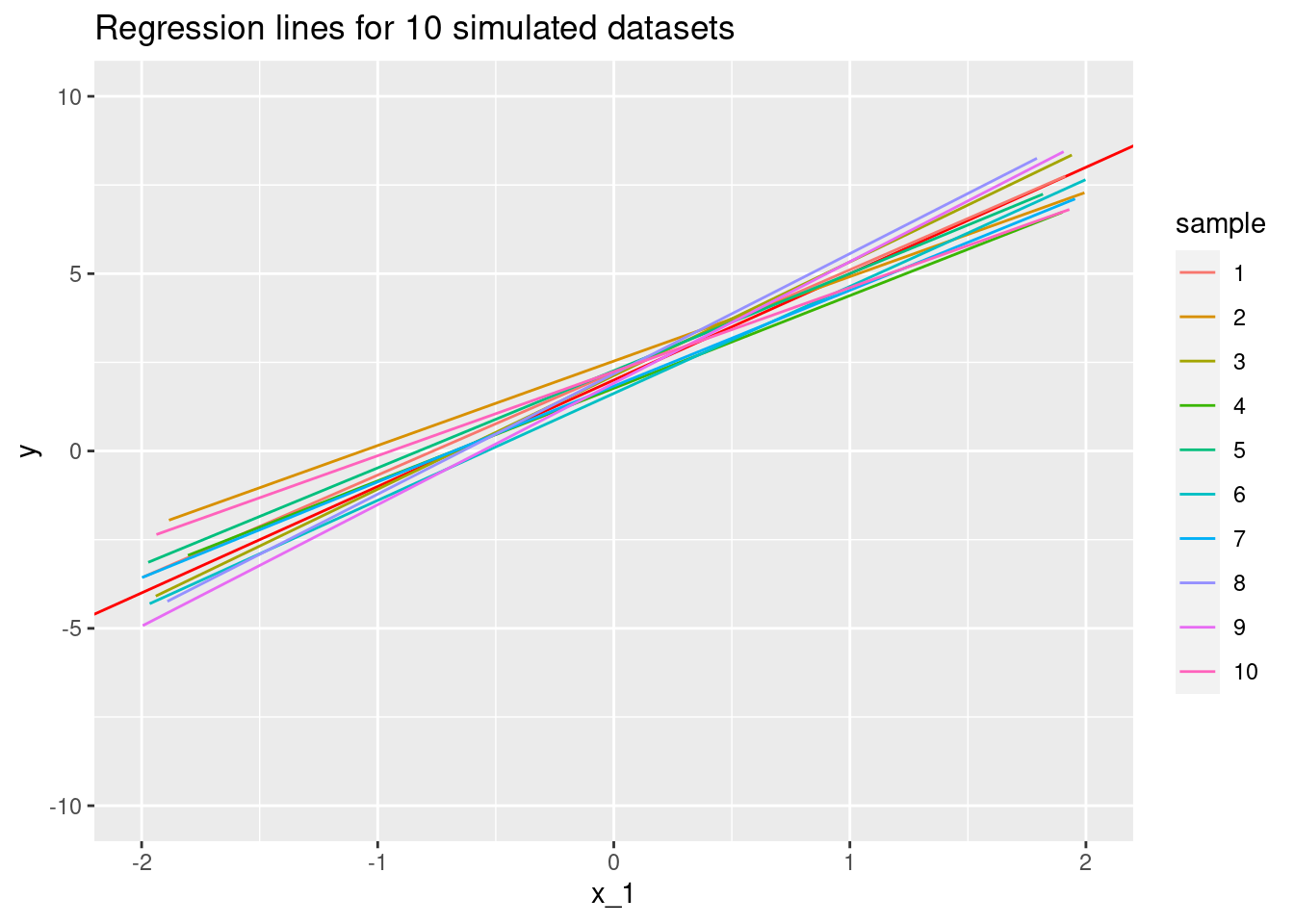

Resampling several times, we find that we end up with several estimated functions (sets of parameters)

# Generate 10 samples and plot

map_df(1:10, ~ simulate_data(beta = c(2, 3), n = 100, sd = 3), .id = "sample") %>%

mutate(sample = as.factor(as.numeric(sample))) %>%

ggplot(mapping = aes(x = x_1, y = y, color = sample)) +

geom_abline(slope = 3, intercept = 2, color = "red") +

geom_smooth(method = "lm", se = FALSE, size = 0.5) +

scale_x_continuous(limits = c(-2, 2)) +

scale_y_continuous(limits = c(-10, 10)) +

labs(title = "Regression lines for 10 simulated datasets")## `geom_smooth()` using formula 'y ~ x'## Warning: Removed 549 rows containing non-finite values (stat_smooth).

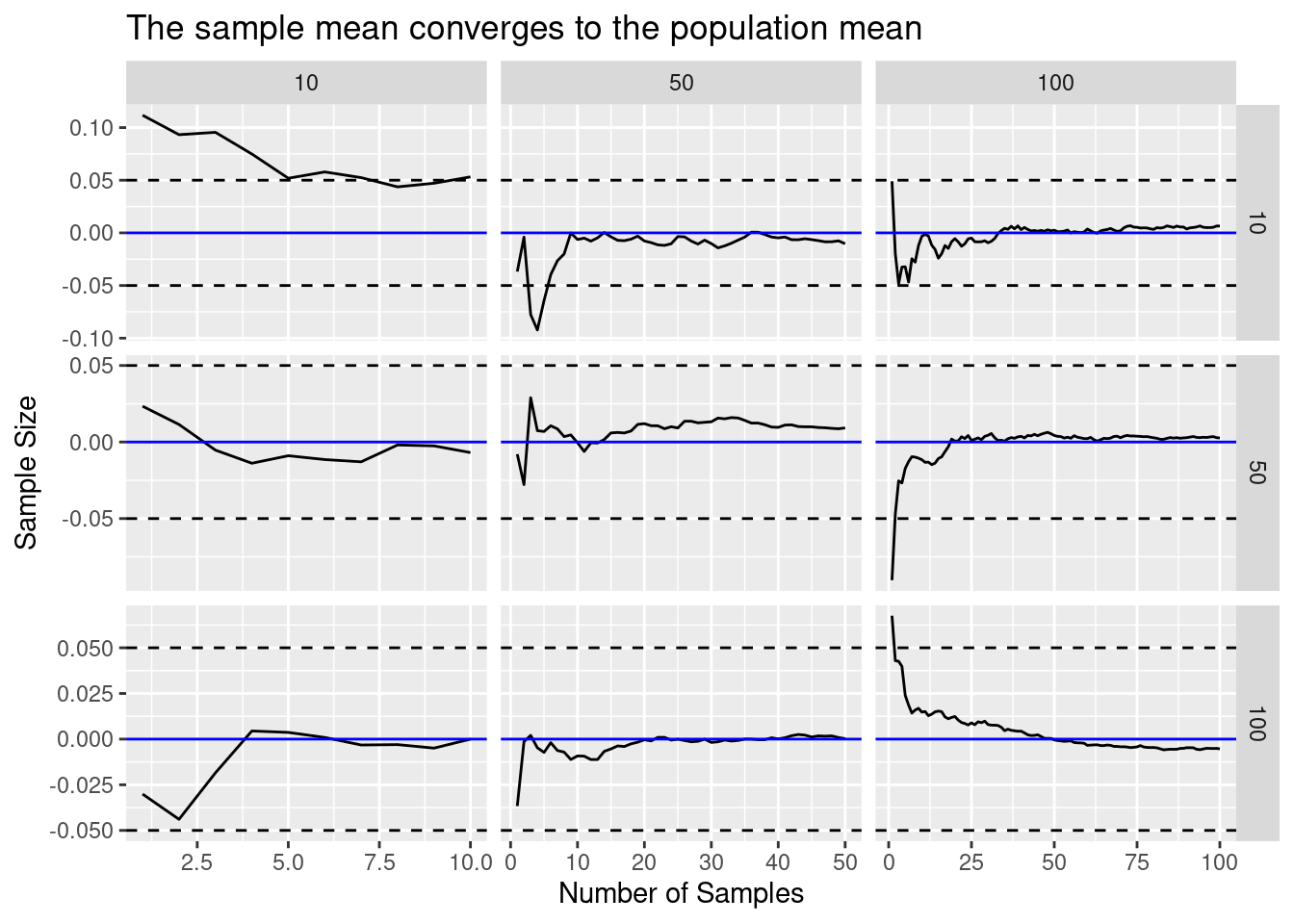

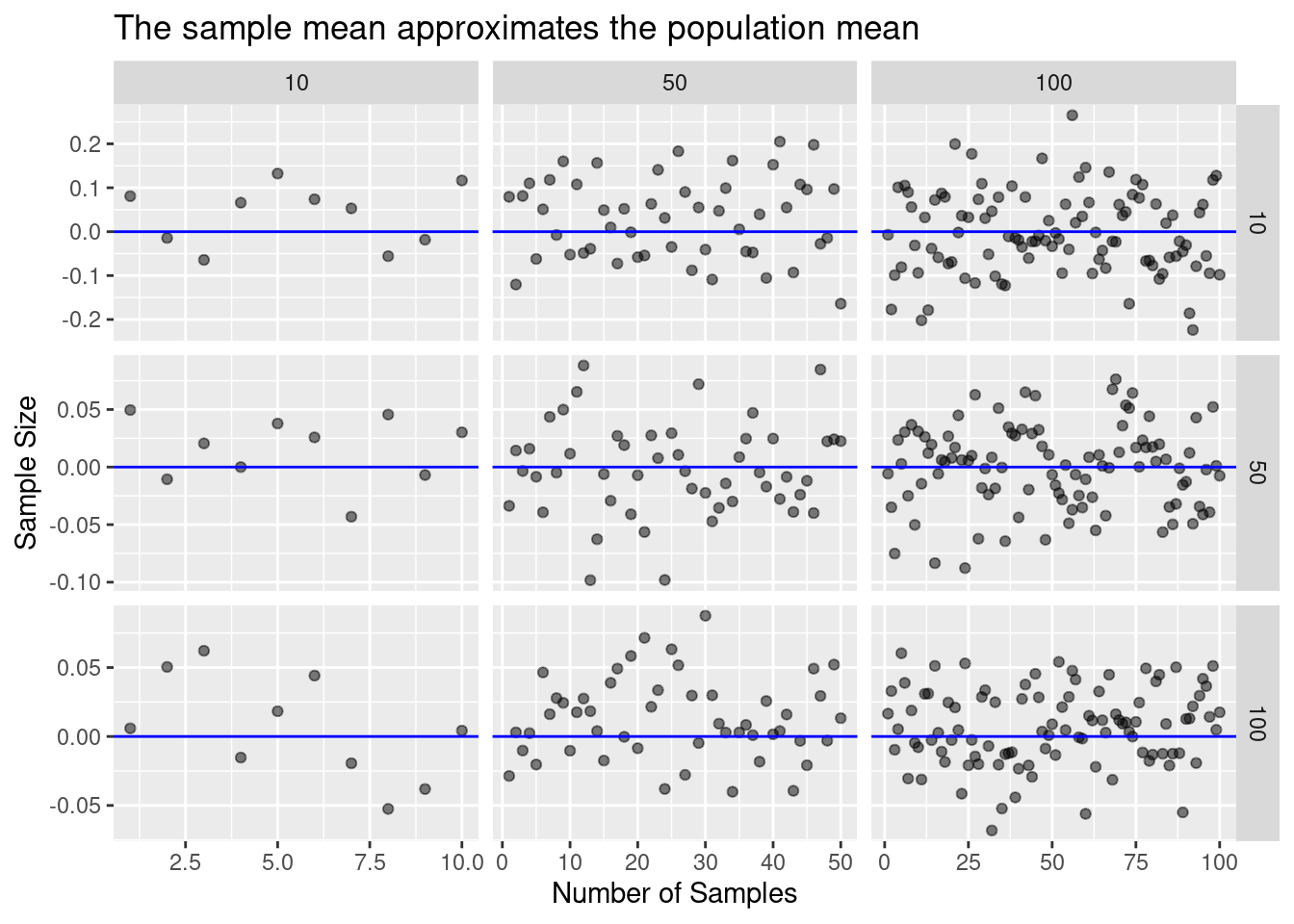

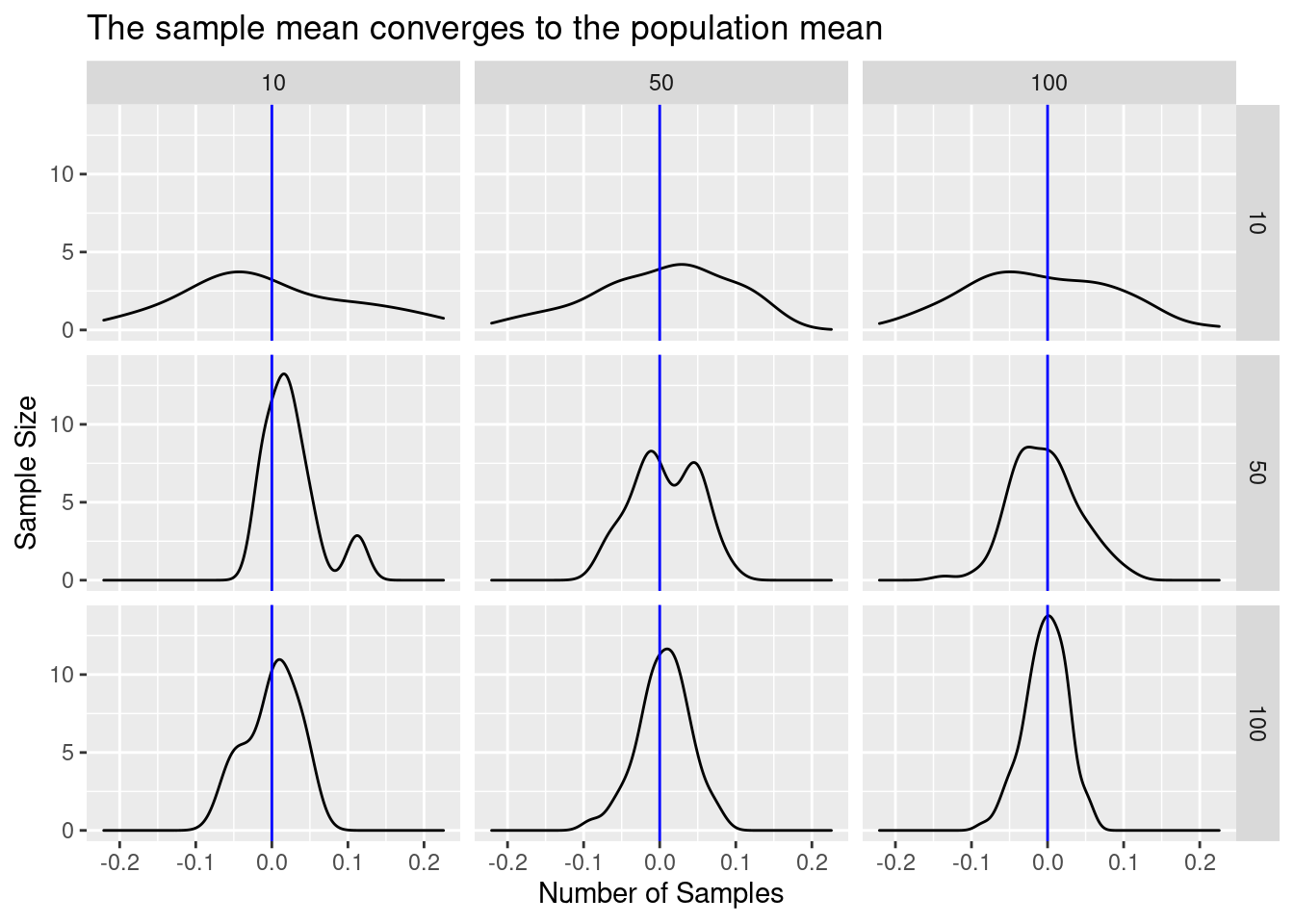

How can we assess accuracy? Statisics!

pmap_dfr(

expand.grid(n = c(10, 50, 100), k = c(10, 50, 100), N = 10000, mean = 0),

generate_sample_means

) %>%

law_of_large_n_gridplot_dots()

pmap_dfr(

expand.grid(n = c(10, 50, 100), k = c(10, 50, 100), N = 10000, mean = 0),

generate_sample_means

) %>%

law_of_large_n_gridplot_density()

pmap_dfr(

expand.grid(n = c(10, 50, 100), k = c(10, 50, 100), N = 10000, mean = 0),

generate_sample_means

) %>%

law_of_large_n_gridplot()